Investing doesn’t stop once you pick your portfolio. Over time, markets move, and your carefully chosen allocation begins to drift. The key question becomes: what if anything should you do about it?

Princeton Asset’s, portfolio backtest tool supports several approaches, each with a different balance of simplicity, discipline, and responsiveness. Here’s a practical guide to understanding them.

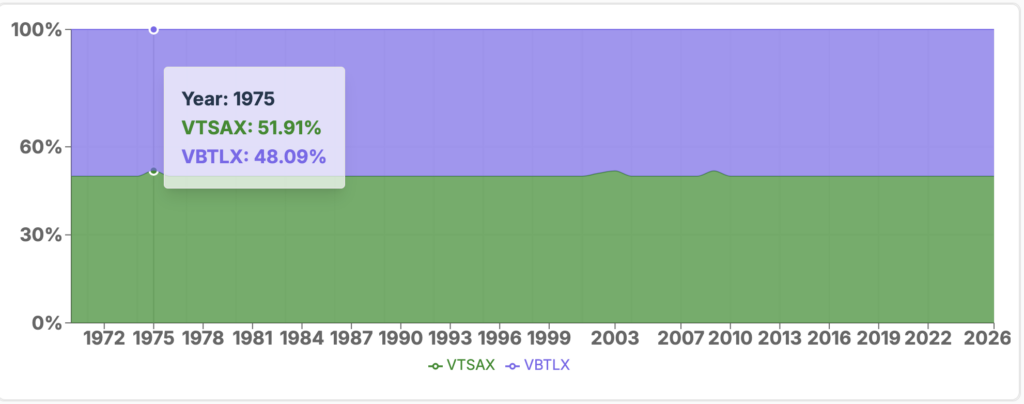

1. Buy and Hold

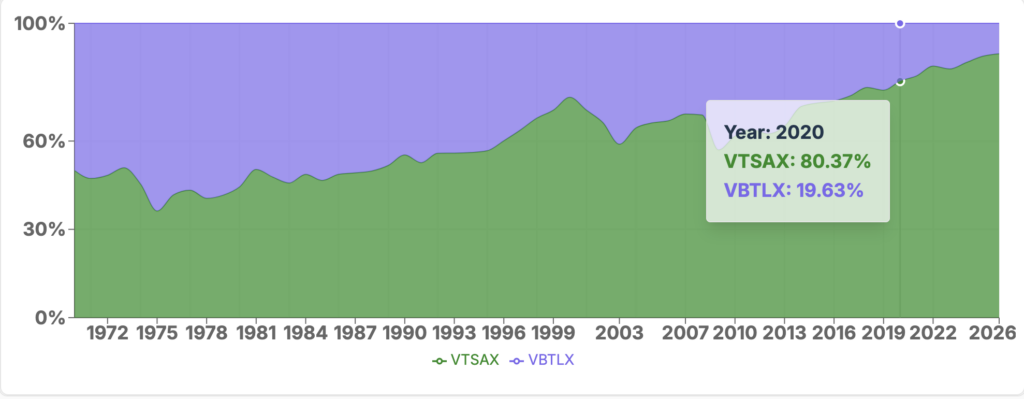

Buy and hold is the simplest strategy: just choose a portfolio and leave it alone.

As markets change, the allocation drifts. If stocks perform well, they will take up a larger share of the portfolio. If bonds lag, they shrink.

Think of it like planting a garden and letting everything grow freely -some plants may take over.

Why investors use it

- No effort required after setup

- Very tax-efficient (no selling)

- Lets strong assets to grow

What to watch out for

- Portfolio can become riskier over time

- May end up overexposed to a single asset class

Example: A 60% stock / 40% bond portfolio might quietly become 80/20 after a period of time with high relative stock to bonds returns.

2. Calendar Rebalancing

Calendar rebalancing brings the portfolio back to its original targets at fixed time intervals.

We support schedules from every 1 year up to every 8 years.

At end of the scheduled rebalancing year the asset allocation weights are reset to original values. In practice you can pick any arbitrary start date as a time measurement reference.

Why investors use it

- Simple and predictable

- Easy to automate

- Keeps risk level consistent over time

What to watch out for

- Markets don’t follow calendars

- Might rebalance too early or too late

Example: If stocks surge right after the yearly rebalance, you’ll wait nearly a full year before adjusting again.

3. Threshold Rebalancing (5/25 Rule)

Instead of using time, threshold rebalancing reacts to how far the portfolio weights have drifted. This rule was formulated by financial theorist and author William Bernstein in his 1996 book, The Intelligent Asset Allocator.

It uses two types of thresholds:

- Absolute: a fixed percentage point change (default ±5%)

- Relative: a percentage of the target weight (default ±25%)

Our portfolio backtest tool allows to adjust threshold values and use one or both thresholds.

How it works

- A rebalance is triggered when an allocation moves “too far” from its target

- Small changes are ignored

Example

Target allocation: 40% in international stocks

- Absolute band: 35% to 45%

- Relative band: also 30% to 50%

When both thresholds are used the one with the smallest deviation is used to trigger the rebalancing action; absolute threshold for the above example. If the allocation moves outside the range chosen for the asset weights threshold(s), we trigger the rebalance action. If not, we leave it alone.

Why investors use it

- Avoids unnecessary trading

- Responds to real market moves

What to watch out for

- Requires frequent monitoring

- Can trigger more trades during volatile periods

4. Symmetric Band Rebalancing (Bogleheads Approach)

This method builds on threshold rebalancing but adjusts the bands symmetrically to 50% allocation and proportional to the size of each allocation.

It is widely discussed in the Bogleheads community (credit to user “longinvest” https://www.bogleheads.org/forum/viewtopic.php?t=186203).

We use a band ratio r = 25% as the default.

Instead of fixed ranges, this method scales the tolerance depending on the allocation size:

- Smaller allocations get tighter control

- Allocations close to 50% get wider bands

- Bands are symmetrical to the middle (50%)

You rebalance when:

Where:

- T – target allocation percentage

- A – actual allocation percentage

- r – band ratio

Example low and high band values to help understanding:

| Target (T) | Low Band (T/(1+r*(1-T)) | High Band (1+r)/(1+r*T) |

| 10% | 8.16% | 12.20% |

| 20% | 16.67% | 23.81% |

| 30% | 25.53% | 34.88% |

| 40% | 34.78% | 45.45% |

| 50% | 44.44% | 55.56% |

| 60% | 54.55% | 65.22% |

| 70% | 65.12% | 74.47% |

| 80% | 76.19% | 83.33% |

| 90% | 87.80% | 91.84% |

Why investors use it

- Adapts naturally to different allocations

- Avoids over-trading small positions

- Backed by a well-tested investing community

What to watch out for

- Slightly more complex than basic rules

5. Overbalancing (Buy the Bear)

For calendar, threshold and band-based methods, we offer an optional enhancement inspired by William Bernstein: overbalancing.

The idea is that instead of just restoring an asset to its target, you add extra weight when the asset has a significant draw down.

Default settings

- Drawdown trigger: 20% decline

- Overbalance ratio: 20% This is multiplied with the draw down to obtain an overbalancing factor.

Example

Your target for stocks is 50%.

A market drop pushes stocks 20% below their last peak.

- Normal rebalance: bring stocks back to 50%

- Overbalance: for 20% draw down and 20% overbalance ratio. Overbalance factor is 1.04 above target asset class weights. 50% -> 52%. After all adjustments weights are normalized to sum to 100%. 50%->52%->50.98%

This strategy encourages buying when prices are lower – something that is psychologically difficult but often claimed to be beneficial long term.

Why investors use it

- Reinforces disciplined “buy low” behavior

- Can improve long-term returns

What to watch out for

- Feels uncomfortable during downturns

- Increases transactions size

Coming Soon: Cash Flow Rebalancing

We are working on adding a more passive approach: cash flow rebalancing.

Instead of selling assets, the portfolio weights are adjusted using:

- Dividends

- New contributions

- Withdrawals

This can reduce taxes and trading while still keeping portfolio allocation on track.

Try It in Practice

Understanding these methods is one thing – seeing how they behave over time is another.

Our portfolio backtest tool lets you test each approach and compare:

- How often rebalancing and overbalancing happens

- How allocations drift

- The impact on risk, returns and other portfolio statistics

If you are building a portfolio or refining your strategy, it is worth exploring which method best matches your goals and your comfort with market swings.

Disclaimer: This blog post is for informational purposes only and should not be considered financial advice. Past performance is not a guarantee of future results. Consult with a qualified financial advisor for personalized guidance.

Leave a Reply