Many investors have heard of tax-loss harvesting, but its lesser-known cousin – tax gain harvesting (TGH) – is often misunderstood. While it might sound appealing to sell appreciated assets to reset your cost basis, the reality is that: over long investment horizons, harvesting gains can actually reduce your after-tax wealth unless your current tax rate is very close to zero.

What is Tax Gain Harvesting?

Tax gain harvesting involves selling investments that have appreciated, paying taxes on the gains now, and immediately repurchasing the same or similar assets. The goal is to reset your cost basis, so that future growth is measured from the new, higher starting point.

It sounds smart – until you consider how taxes today interact with compounding over decades.

Why You Need to Be Cautious

Paying taxes today reduces the compounding base. Over long periods, this can outweigh any future tax savings from resetting your basis. Even modest current tax rates can make harvesting counterproductive.

The key takeaway: unless your current effective tax rate on gains (TI) is close to zero, harvesting gains over long horizons can make you worse off than simply deferring the gain.

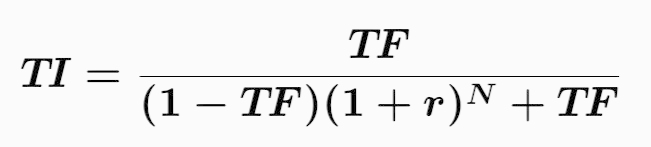

The Breakeven Formula

Mathematically, the breakeven current tax rate TI – the effective tax rate at which harvesting now is neutral compared to deferring – is:

Where:

- r = expected annual return

- N = years until final sale

- TF = future effective long-term capital gains tax rate

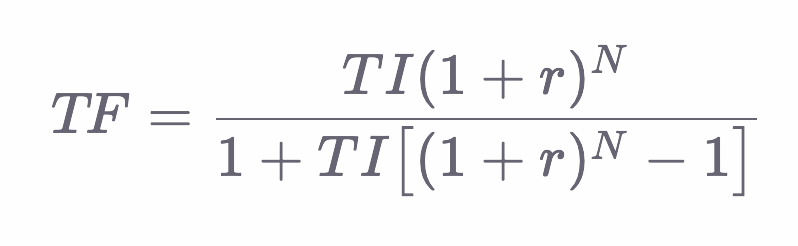

And the reverse formula:

How to Read the Formula

- As N or r increase, the denominator grows faster than the numerator, meaning TI must approach zero for harvesting to be worthwhile.

- Even a small current tax rate today can destroy decades of compounding, leaving you worse off than if you had deferred the gain.

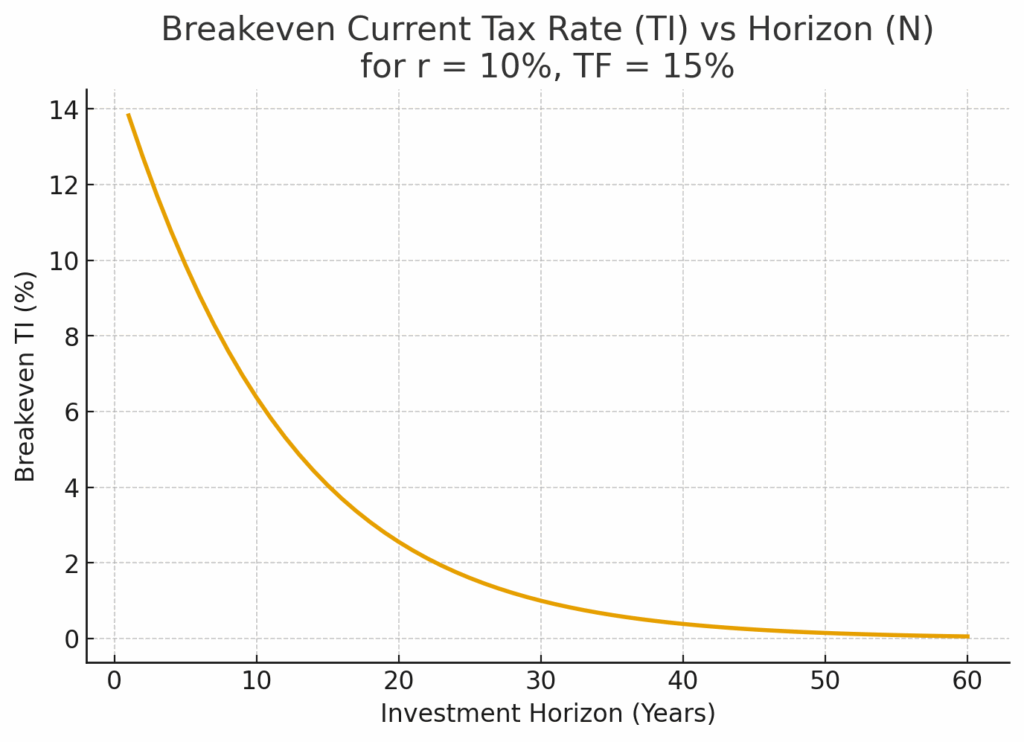

Example

Suppose you hold a fully appreciated stock expected to grow at 10% per year over 30 years, with a future effective long-term capital gains tax rate of 15%.

- Using the formula above, the breakeven TI is 1%.

- This means that if your current tax rate is even slightly above that, harvesting gains today would reduce your long-term wealth compared to simply letting the investment grow.

The longer your horizon, the lower TI must be – in practice, to be safe it should be zero for decades-long holdings.

The Bottom Line

Tax gain harvesting is not inherently “free money”.

Over long horizons:

- Paying taxes today reduces the compounding base.

- Even modest current tax rates can make harvesting detrimental.

- Only in truly low-tax years (TI ≈ 0%) does harvesting gains make practical sense.

Caution: Do not harvest gains over long periods unless your current effective tax rate is zero. Otherwise, you risk losing money compared to simply deferring the gain.

In most states the taxes applied to long term capital gains would render the Tax Gain Harvesting unusable over long time horizons.

Finally, TI and TF represent not just the capital gain rates applied to the sale but the effective tax percentage, which, due to the increase of MAGI, can include the loss of tax credits and increases in healthcare insurance costs. For example, a realized gain immediately impacts the ACA Premium Tax Credit (upon reconciliation in the same tax year), but the increased MAGI can also cause a Medicare IRMAA surcharge that is delayed by two years (a gain realized in year t affects your premium in year t+2). To get a realistic sense of these comprehensive, blended marginal tax rates – including both immediate and delayed consequences – it is best to use a tax calculator that shows the sale’s true cost.

We hope that this will help investors navigate these complex trade-offs and design truly tax-efficient strategies that protect long-term wealth.

Disclaimer: This blog post is for informational purposes only and should not be considered financial advice. Consult with a qualified financial advisor for personalized guidance.

Leave a Reply