The 2025 One Big Beautiful Bill Act (OBBBA) reform was intended to make one of the biggest changes to Social Security taxation in decades. Most commentary focuses on the headline feature – eliminating the taxation of Social Security benefits for the majority of retirees – but the real story sits deeper in the details.

OBBBA increases the standard deduction, leaves unchanged the over-65 deduction, and adds a new additional senior bonus deduction. This creates a surprising pattern of tax savings across income levels. For some retirees, the tax break is big. For others, it fades out almost completely.

And unexpectedly, the largest proportional tax benefit appears around $150,000 of gross income – not at the low end of the income spectrum.

Let’s break down what changes, why it matters, and what the numbers reveal.

1. Standard Deductions Before and After OBBBA

Before OBBBA (under current 2025 rules), a married couple filing jointly receives:

- A standard deduction

- An additional deduction for each spouse age 65+

This senior deduction has long existed to prevent retirees – who typically rely on Social Security and modest withdrawals – from being taxed on what policymakers historically considered subsistence income.

What OBBBA Changes

Under OBBBA, beginning in 2025:

- Standard Deduction: increases to $31,500 from $30,000 (MFJ)

- Age Deduction: $1,600 remains the same.

- New Additional Senior Bonus Deduction: $6,000 per person age 65+

- However, the additional deduction is subject to phase-out limitations:

- Phaseout starts at $75,000 MAGI (single) / $150,000 MAGI (married)

- Fully phased out at $175,000 (single) / $250,000 (married)

In other words:

A retired married couple over age 65 can get up to $15,200 in combined deductions —

but lose the entire $12,000 additional senior deduction if MAGI exceeds $250,000.

This detail combined with the federal tax brackets turns out to be critical to understanding why OBBBA tax savings stay flat between 100-150K gross income and then drop sharply at higher incomes.

2. Why the Senior Deduction Exists

The original intent behind the over-65 deduction was to:

- Reduce tax liability for retirees living largely on Social Security

- Offset the taxation of Social Security benefits that slowly expanded over decades

- Simplify filing for older Americans by anchoring them below filing thresholds

The OBBBA initially attempted to fix the root problem by eliminating the tax on Social Security benefits:

Its stated intent was to eliminate the taxation of Social Security benefits, making the old patchwork senior deduction less necessary.

However, the law that was enacted (OBBBA) was only able to add yet another additional deduction for people over 65. But because the new additional deduction phases out, the benefit curve looks strange – zero savings at low income, strong savings at mid-income, and modest savings at high income.

This difference – “tax eliminated directly” vs “deduction offsets income” – is subtle but important, because it affects how other income (e.g. IRA withdrawals, investment income) interacts with Social Security taxation.

3. How Many Retired Couples Actually Have $100K+ Gross Income?

This question matters because our analysis shows the biggest OBBBA Social Security tax offset occurs below $100,000 of gross income. So how many retirees are even in that zone?

Using recent household-income distribution data and adjusting to 2025 dollars:

Approximately 30% to 35% of couples aged 65+ receiving Social Security will have gross income over $100,000 in 2025.

This estimate is based on:

- Senior mean household income of ~$75,000 (2023) – significantly higher than the median

- A long right-tail income distribution among retirees

- Inflation adjustments from 2023→2025 (~6.06%)

- SSA and Census findings showing ~30%+ of senior households already above the equivalent of $100K

This validates that the modeled below-$100K gross income range is not a fringe case – a meaningful portion of retirees (65-70%) are in it .

4. Running the Numbers: A 66-Year-Old Couple in 2025

Using the charted scenario:

- Social Security: $50,000 (close to the national average for a couple)

- Add Traditional IRA withdrawals in $10,000 increments

- Measure the tax savings before vs. after OBBBA

Here’s what happens:

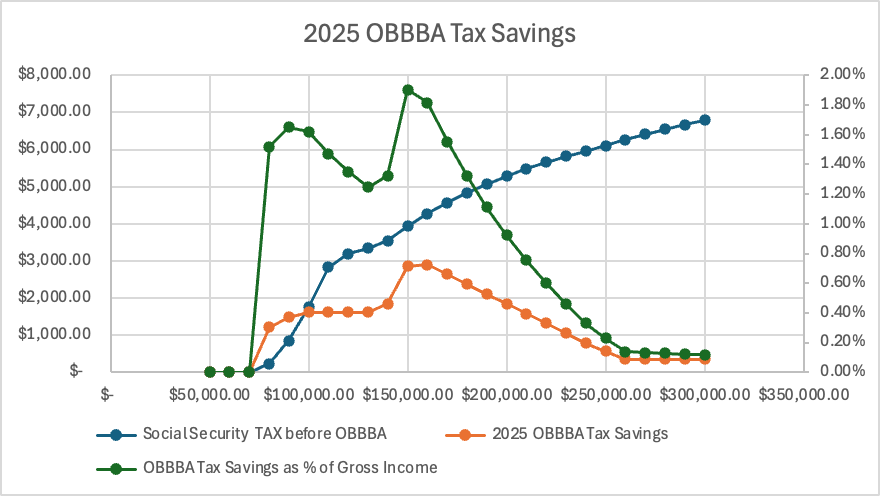

A. Social Security Tax is Offset Until ~$100K Gross Income

Under current law (pre-OBBBA):

- 50–85% of Social Security becomes taxable once provisional income rises

Under OBBBA:

Social Security taxation is eliminated until gross income exceeds roughly $100,000.

This creates the promised savings for households with gross income under $100K. However, it applies mostly for the gross income range of 70-100K, because Social Security benefits were not taxed below $70K anyway.

Between $100K and $150K of income, the federal bracket stays at 12%, but the share of Social Security that is taxed keeps rising, which is why the 2025 OBBBA tax‑savings (orange-line) appears flat in that range.

B. Maximum Percentage Savings at ~$150K Gross Income

This surprisingly steep peak in your analysis happens because:

- There is a jump to 22% federal tax bracket

- The couple still receives the full $6,000 per-person deduction

- This additional senior deduction has not yet started to phase out

This unique combination creates

The highest tax savings as a percentage of gross income, at around $150,000, of 1.9%.

C. OBBBA Savings Collapse Above $250,000 Gross Income

Once MAGI > $250K:

- The entire $12,000 additional senior deduction disappears

- Ordinary taxes dominate

- Only the base changes in standard deduction contribute to the difference

This is why:

For gross incomes above $250K, OBBBA tax savings shrink to about $360.

One can visualize this on the chart: a dramatic drop-off once the $250K phaseout threshold is reached.

5. What This Means for Retirees

1. Middle-income retirees win big.

Incomes between ~$80K and ~$220K see a strong proportional benefit. No change for retirees below the 70K gross income range. And a sloped asymptotic decline for retirees with gross income above $220K.

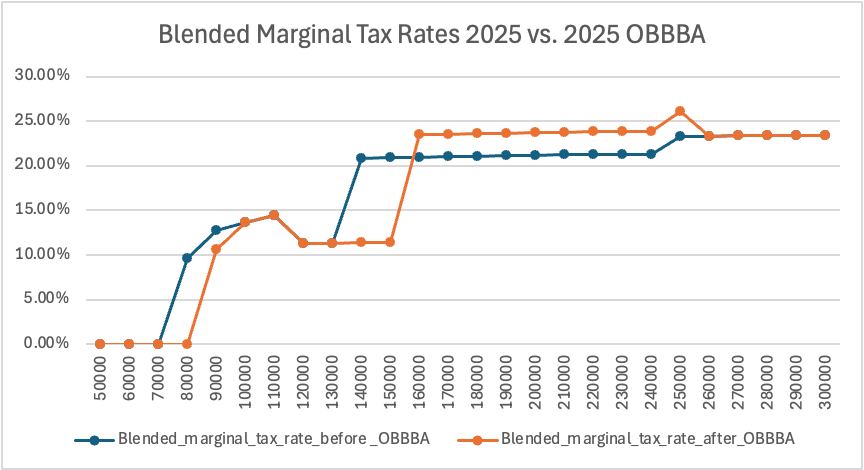

2. The “tax torpedo” is narrowed.

Reducing Social Security taxation shifts the marginal rates to higher incomes and narrows the initial tax torpedo to the 95->120K range from 85->120K, and creates a new mini torpedo in the 240-250K range.

3. Higher-income retirees still benefit — but modestly.

After $250K, savings flatten to about $360.

4. The OBBBA phaseout creates a sharp cliff.

The new additional senior deduction is generous at lower incomes but turns off quickly, creating the distinctive spike in savings.

5. The longevity of the benefit is temporary (2025–2028)

As many analyses note, the extra $6,000 deduction (the “senior bonus”) is scheduled to expire after 2028 unless extended.

That’s relevant for long-term planning. Retirees using this to shape IRA withdrawals or Roth conversion strategies should consider that the window is limited.

Final Thoughts

The OBBBA reform dramatically reshapes the retiree tax landscape – not by eliminating the taxation of Social Security, but by redesigning how deductions work for seniors.

Our analysis reveals something counterintuitive but important:

The largest proportional OBBBA tax savings don’t go to the lowest-income or highest-income retirees — but to the middle-upper bracket in the $80K-$150K range.

Because as many as one-third of senior couples fall above the $100K income mark, this effect is far from theoretical.

For the retired couple with average Social security Income:

– if total income under $70K: no change.

– In 70-100K range: tax savings are greater than before OBBBA (due to reduced Social Security tax).

– At 150K: maximum relative benefit in effective and marginal tax rate (similar to the pre‑OBBBA case at around $90K of income).

Raw data from: 2025 tax BEFORE OBBBA and 2025 tax AFTER OBBBA

Disclaimer: This blog post is for informational purposes only and should not be considered financial advice. Consult with a qualified financial advisor for personalized guidance.

Leave a Reply