When planning a Roth conversion, it’s easy to focus only on the income tax impact. But if you’re on ACA health insurance or Medicare, the conversion can also trigger changes in your ACA subsidies and IRMAA surcharges.

In this example, we’ll quantify:

The tax you’ll pay for the Roth conversion.

The additional ACA premiums you’ll owe.

Any IRMAA surcharges that apply.

Problem Setup

We compare two scenarios:

Base Case – No Roth conversion.

Conversion Case – Roth conversion of $65,000.

Our goal is to measure how much more we’ll pay in taxes and premiums in the conversion case compared to the base case.

Base Income Scenario

Household

John (65) – Medicare

Jane (60) – ACA

Location: New Jersey

Base income: $60,000

$10,000 – 1099 income (Jane self-employment)

$10,000 – Qualified dividends

$10,000 – Long-term capital gains

$30,000 – Pension (John)

ACA Premium Reference To compute ACA premiums, we also need the SLCSP (Second Lowest Cost Silver Plan). Using the KFF Subsidy Calculator, we get:

ACA SLCSP = $12,877

Note: “Tax Input” fields have a sub-label: “Earned Income”, “Principal”, etc… if the income type you want to enter is not listed in one of the input fields then please read this blog post and then add that income to one of the input fields of the same category

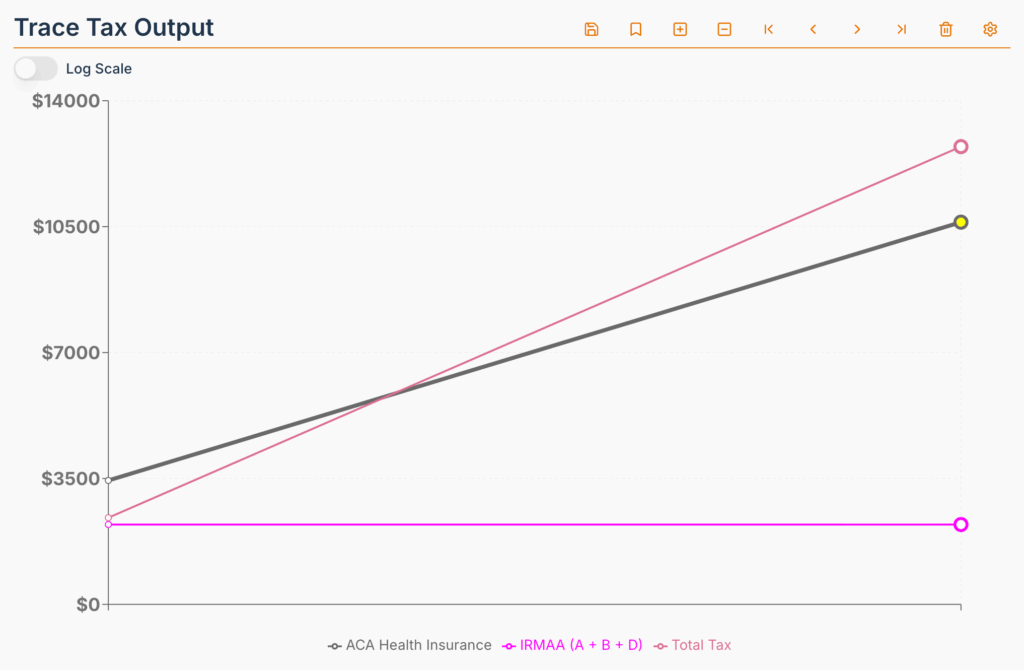

Base Case Tax Output:

ACA Health Insurance: $3,445.01

IRMAA (A + B + D): $2,220.00

Total Tax: $2,408.81

Tip: In our tax calculator, scroll to the chart at the bottom and click [+] to add this tax point to the trace.

Then click the gear icon and select: “ACA Health Insurance”, “IRMAA (A + B + D)”, and “Total Tax” to track them over the two tax scenarios.

Roth Conversion Scenario

We add $65,000 in Roth conversion income by increasing the TIRA Withdrawal field from $30,000 to $95,000.

Conversion Case Tax Output:

ACA Health Insurance: $10,625.00

IRMAA (A + B + D): $2,220.00

Total Tax: $12,724.68

Tip: Scroll to the chart and click [+] to add this point to the trace.

You can switch between input scenarios by double-clicking on any point in the chart.

Quantifying the Roth Conversion “Cost”

Category

Conversion Case

Base Case

Additional Cost

ACA Health Insurance

$10,625.00

$3,445.01

$7,179.99

IRMAA (A + B + D)

$2,220.00

$2,220.00

$0.00

Total Tax

$12,724.68

$2,408.81

$10,315.87

Total Additional Cost: $7,179.99 (ACA) + $10,315.87 (Tax) = $17,495.86

ACA subsidies are based on current year (t) ACA MAGI so current year ACA Premiums will increase by the above amount.

IRMAA surcharges are based on (t-2) IRMAA MAGI so the year after next one your IRMAA premiums will increase by the above amount.

A Roth conversion in 2026 might be subject to the old 400% ACA cliff, leading to an even worse outcome.

Key Takeaways

ACA healthcare premiums can be increased significantly by Roth conversions, especially before Medicare eligibility.

IRMAA surcharges may not always be affected, but when they are, they can add thousands to your annual costs.

Always evaluate total impact of taxes plus lost subsidies before deciding on the conversion amount.

Disclaimer:This blog post is for informational purposes only and should not be considered financial advice. Consult with a qualified financial advisor for personalized guidance.

One response to “How Roth Conversions Affect ACA and IRMAA Subsidies”

Michael

You are doing something that no one else is doing. Creating a calculator to figure this out. Personally I’m tired of listening to CFP’s, that are trying to get my business, telling me I need to do Roth conversions now. I tell them that I have a spouse and two minor children on the ACA and we are getting premium tax credits of about $19,000/Year and that needs to be accounted for BEFORE I commit to Roth conversions. Their eyes glaze over like I’m the only person that has this issue and they all tell me they can’t figure it out.

Leave a Reply