If you’re enrolled in Medicare, you may have encountered the term IRMAA – the Income-Related Monthly Adjustment Amount. This additional premium can significantly impact your Medicare costs, but understanding how it works and knowing about potential discounts can help you better manage your healthcare expenses.

What is IRMAA?

IRMAA is an extra charge added to your Medicare Part B and Part D premiums if your IRMAA modified adjusted gross income (MAGI) exceeds certain thresholds. One crucial detail that many beneficiaries don’t realize is that Medicare looks at your IRMAA MAGI from two years ago (t-2) to determine your IRMAA status.

Life-Changing Events That Can Help Reduce IRMAA

Medicare recognizes that certain life events can significantly impact your income. You can file for an IRMAA reduction if you experience any of these qualifying life-changing events:

- Marriage

- Divorce/Annulment

- Death of a spouse

- Work reduction or stoppage

- Loss of income-producing property due to a disaster or other event beyond your control

- Loss or reduction of pension income

- Employer settlement payment due to employer’s bankruptcy

How to Request an IRMAA Reduction

If you’ve experienced any of these life events and your current income is lower than what Medicare is using to calculate your IRMAA, you can:

- Fill out Form SSA-44 (Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event)

- Provide documentation of your life-changing event

- Submit proof of your reduced income

- Submit these materials to your local Social Security office

Planning Strategies to Minimize IRMAA

Consider these strategies to manage your IRMAA exposure:

- Time your income recognition carefully in retirement

- Consider Roth conversions in lower-income years

- Manage required minimum distributions (RMDs) strategically

- Use qualified charitable distributions (QCDs) to reduce your MAGI

- Structure retirement withdrawals to stay below IRMAA thresholds

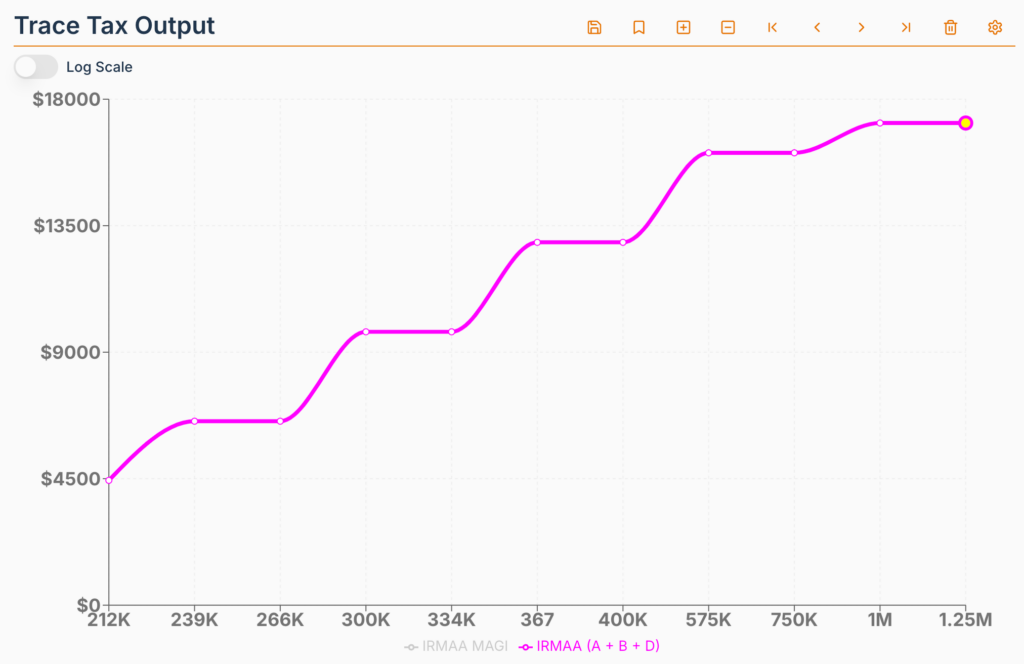

Fig. 1. Medicare B+D premiums in 2025 as a function of (2023, t-2) IRMAA MAGI for a Married Filling Jointly couple using our income tax calculator.

Important Reminders

- IRMAA determinations are made annually

- The two-year lookback period means planning ahead is crucial

- Appeals must be filed within 60 days of receiving your IRMAA determination

- New Medicare enrollees should plan for potential IRMAA impacts before enrollment

Conclusion

While IRMAA can be a significant additional expense for higher-income Medicare beneficiaries, understanding the thresholds, qualifying life events, and available planning strategies can help you manage these costs effectively. Regular review of your income situation and proactive planning with your financial advisor can help minimize your IRMAA exposure while ensuring you maintain appropriate Medicare coverage.

Disclaimer: This blog post is for informational purposes only and should not be considered financial advice. Consult with a qualified financial advisor for personalized guidance.

Leave a Reply