The Affordable Care Act (ACA) provides health insurance subsidies to help lower-income individuals and families afford coverage. These subsidies are determined based on a taxpayer’s income and the cost of health plans available in their area. Understanding how ACA subsidies work, particularly the role of Modified Adjusted Gross Income (MAGI) and the benchmark silver plan, will help you plan for health insurance costs.

The role of MAGI in ACA subsidies

ACA subsidies are based on your Modified Adjusted Gross Income (ACA MAGI), with a key administrative distinction. For initial enrollment and to receive the monthly Advance Premium Tax Credit (APTC), the Marketplace typically uses your prior tax year’s (t-1) ACA MAGI (e.g., your 2024 MAGI for 2025 coverage) to estimate your payment. However, the final, definitive subsidy amount you are actually entitled to is based on your actual ACA MAGI for the current coverage year (t).

How is ACA MAGI calculated?

MAGI starts with your Adjusted Gross Income (AGI) from your tax return and then adds back certain deductions, including:

- Non-taxable Social Security benefits

- Tax-exempt interest

- Foreign earned income exclusions

Your MAGI determines whether you qualify for Premium Tax Credits (PTCs) and Cost-Sharing Reductions (CSRs), which help reduce your monthly premium and out-of-pocket healthcare expenses, respectively.

Current Year Actual MAGI (e.g., 2025 MAGI on your tax return) is the income used for final reconciliation.

When you file your 2025 tax return in early 2026, you report your actual 2025 ACA MAGI.

The IRS compares the total APTC that was paid on your behalf throughout 2025 against the final Premium Tax Credit (PTC) you were actually eligible for based on your final 2025 income.

Reconciliation:

- If you underestimated your 2025 MAGI (and received too much APTC), you may have to repay some or all of the excess subsidy.

- If you overestimated your 2025 MAGI (and received too little APTC), you will receive the difference as a tax refund.

Crucial Advice: The most important thing is to update your Marketplace application promptly throughout the year if your current year’s estimated MAGI changes significantly to minimize repayment or refund surprises during tax filing.

The benchmark plan and how it affects subsidies

ACA subsidies are tied to the cost of Second Lowest Cost Silver Plan (SLCSP) available in your marketplace. The government sets a maximum percentage of your income that you’re expected to pay for this benchmark plan, and the subsidy covers the rest.

How it works:

- The marketplace calculates the cost of the SLCSP in your area.

- The expected contribution is determined based on your MAGI as a percentage of the Federal Poverty Level (FPL) for your family size.

- The subsidy amount is the difference between the cost of the SLCSP and your expected contribution.

How to estimate the SLCSP

To estimate your ACA subsidy, you need to find the cost of the SLCSP in your area. Here’s how:

- Visit Healthcare.gov (or your state’s ACA marketplace if applicable) and enter your ZIP code.

- Browse silver plan options and look for the SLCSP available.

- Use an ACA subsidy calculator, such as those provided on Healthcare.gov, healthsherpa.com, Kaiser Family Foundation 2025 or Kaiser Family Foundation 2026 without enhanced subsidies, input your MAGI and household details for an estimate.

Key takeaways

- Your MAGI from the prior tax year (t-1) is used by the Marketplace to approve and estimate your monthly Advance Premium Tax Credit (APTC). However, remember that the final subsidy is determined by your actual MAGI for the coverage year (t) and is reconciled with the IRS when you file taxes. Planning for MAGI adjustments is crucial to avoid a repayment of excess subsidies.

- The subsidy amount is based on the SLCSP in your area.

- You can estimate your subsidy by using Princeton Asset’s income tax calculator.

- Planning for MAGI adjustments can help optimize your subsidy eligibility.

Understanding these key factors ensures you receive the maximum available assistance for health coverage. If you need a more precise estimate, using our online income tax calculator or speaking with a tax professional can help tailor the results to your financial situation.

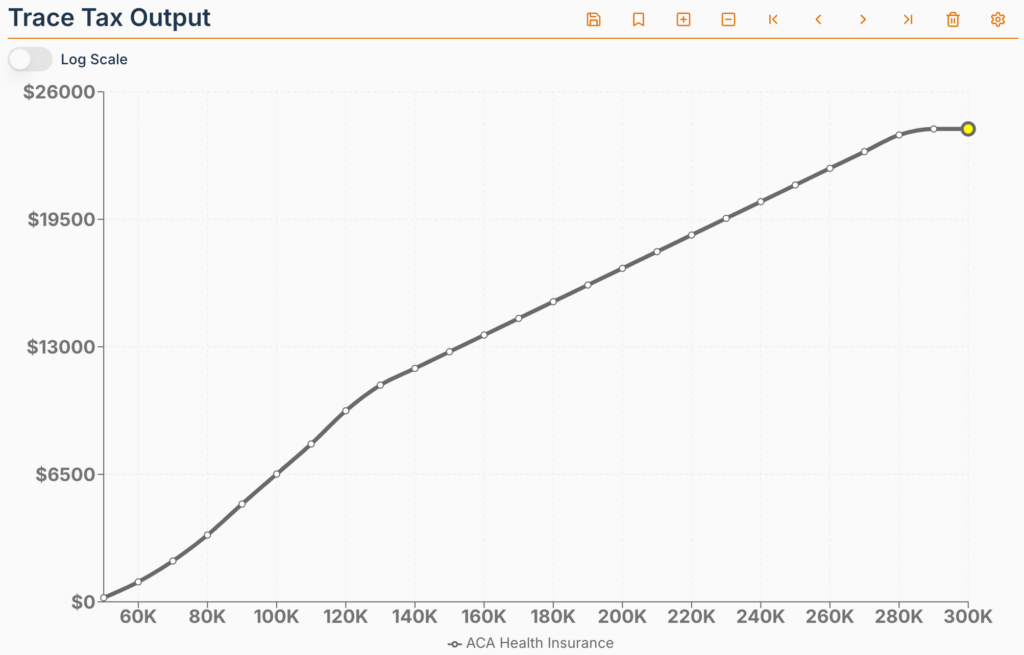

Fig. 1. Example cost of ACA health insurance for a family of 2 (51 year old non-smoking) adults with 2 (non-smoking) children in NJ. The Kaiser Family Foundation estimates the SLCSP to be $24,108.00 per year and with our income tax calculator you can plot the ACA healthcare insurance cost for a 2025 MAGI from $50K to $300K.

PS. ACA “Subsidy Cliff” expiration

Currently: People above 400% FPL can still receive subsidies.

Future (if no action): The subsidy cliff will return, and subsidies will be lost for those with MAGI above 400% FPL.

Disclaimer: This blog post is for informational purposes only and should not be considered financial advice. Consult with a qualified financial advisor for personalized guidance.

Leave a Reply